Thanks to PMXT for providing this data for free!

New in Version 2:

- Nautilus 1.225.0, via PyPI in lieu of a subtree

- Better backtest runner classes via EXPERIMENT objects

- IPython notebook support (.ipynb files)

- Joint portfolio multi replay runners

- Growing support for statistical optimizers

- New aggregate charts

- Massive improvements charting gen speed

- an attempt at a Tree-structured Parzen Estimator via Optuna

Looking for the old version? That was renamed to Version 1

Backtesting framework for prediction market strategies on Kalshi and Polymarket, built on top of NautilusTrader with custom exchange adapters. Plotting inspired by minitrade. This repo is still in active development.

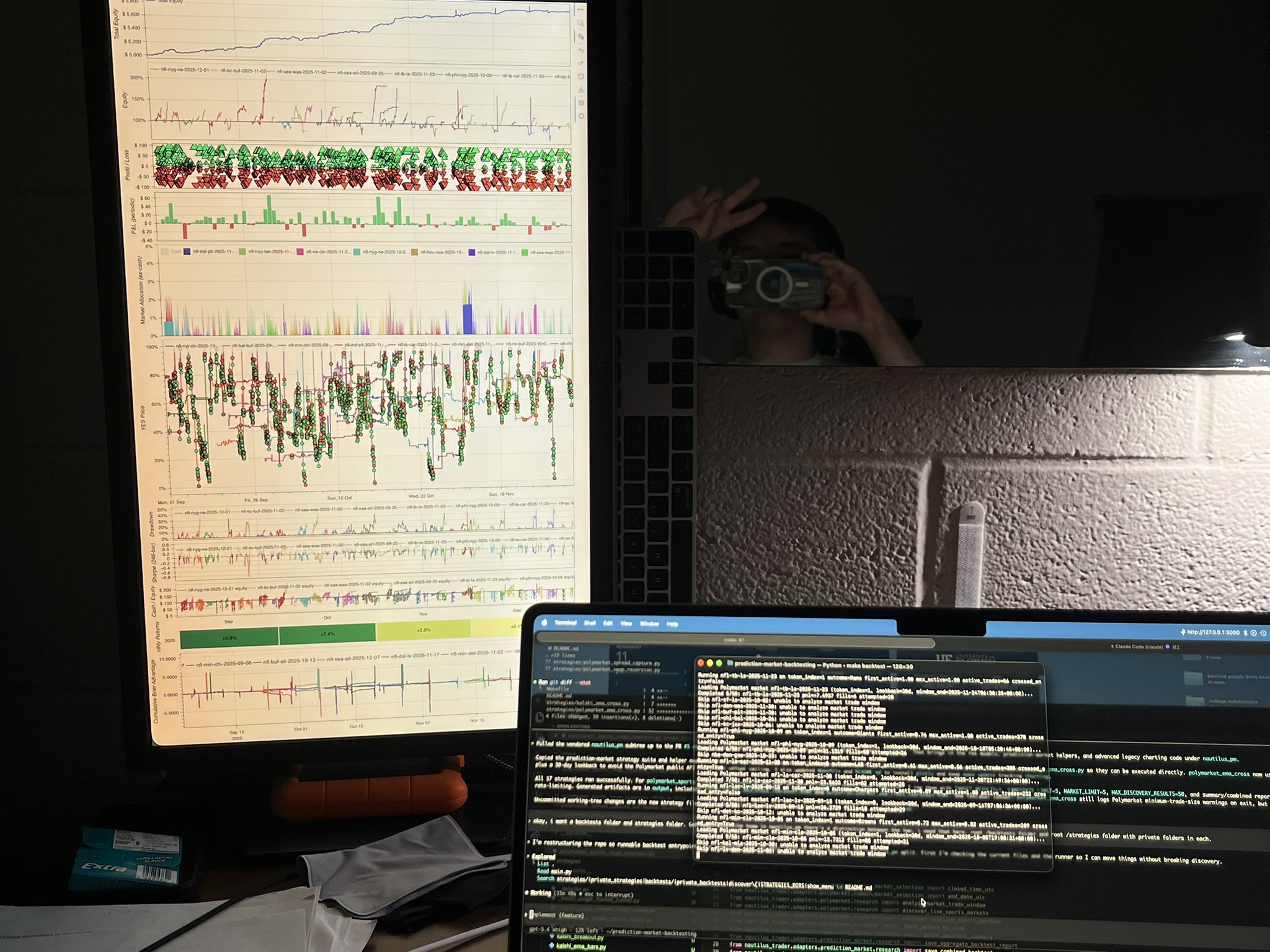

Fantastic single & multi-market charting. Featuring: equity (total & individual markets), profit / loss ticks, P&L periodic bars, market allocation, YES price (with green buy and red sell fills), drawdown, sharpe (with above/below shading), cash / equity, monthly returns, and cumulative brier advantage.

If you find any bugs, unexpected behavior, or missing simulation features, PLEASE post an issue or discussion.

Detailed guides have been filed away in the docs index for better organization and long-term sustainability.

- Docs Index

- Setup

- Backtests And Runners

- Research

- Execution Modeling

- Data Vendors, Local Mirrors, And Raw PMXT

- Mirror And Relay Ops

- Vendor Fetch Sources And Timing

- Plotting

- Testing

- Project Status

- License Notes